The value of customs duties paid by UK businesses increased by 64% to £4.5 billion in the 12 months to 31st January, revealing the full impact of post-Brexit rules on trade for the first time.

One year on from the UK’s departure from the EU’s single market and customs union, British businesses are paying more import and export taxes than at any point in history and the last five months to January 2022 were the five highest individual months on record for customs duties.

Research by UHY Hacker Young found the total of £4.5 billion was up from £2.9 billion in the previous 12-month period.

Experts suggested the spike in recent months could have been accelerated by the earlier decision of some businesses to defer customs declarations due to the growing administrative burden placed on them by Brexit.

What are the post-Brexit rules on imports?

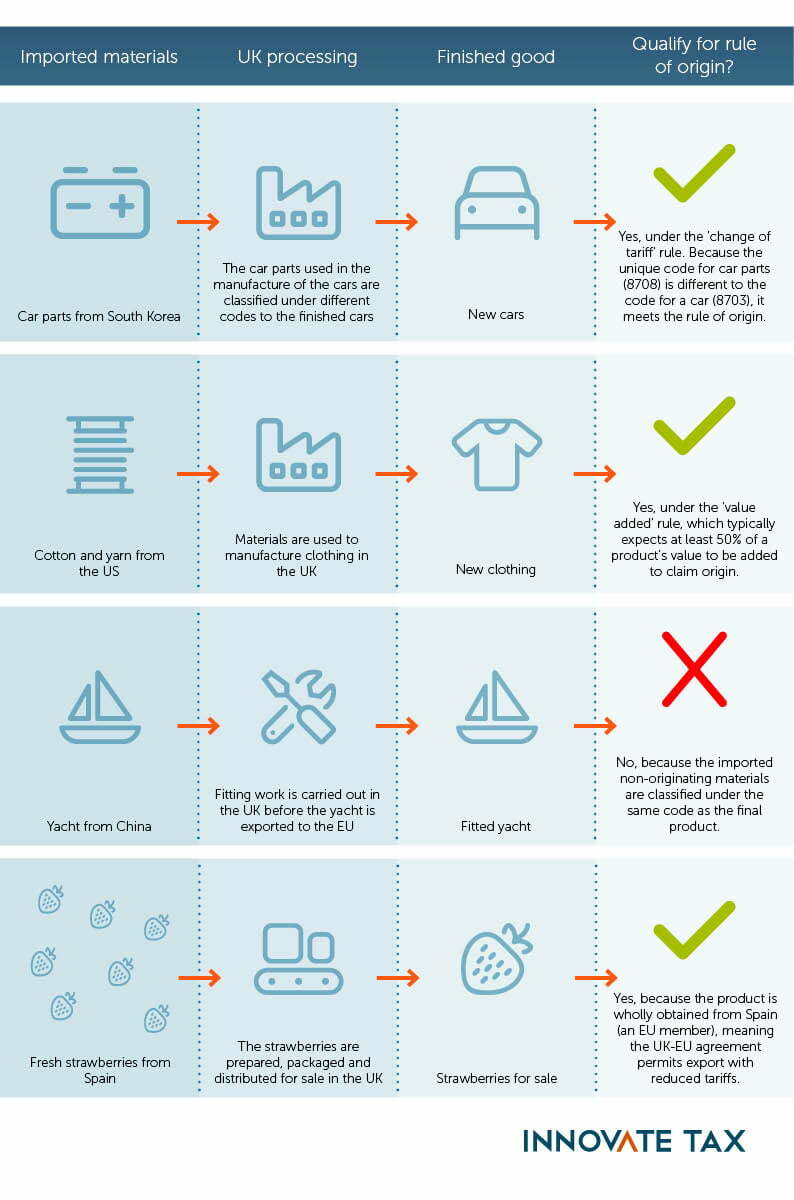

Under the Trade and Cooperation Agreement agreed by the UK and EU, goods must meet new ‘rules of origin’ requirements to qualify for exemption from customs duties.

This means there must be a satisfactory level of processing of a product within the country of export for a business to access zero tariffs upon exporting it. Businesses must meet at least one criteria to justify significant processing in a particular country – such as adding more than 50% of value to imported materials or changing their use – and subsequently claim reduced customs duties.

The rule of origin sets out to determine the principle origin of goods based on where the products or materials used in their production come from.

Ultimately, a reduced rate of customs duty can only be applied to goods that are proven to originate in the UK or EU – and not from outside countries.

Goods that do not meet the rules of origin can still be traded between the UK and EU but will not be liable for a reduced rate of customs duty. In such cases, businesses will have to pay the standard tariff that the UK and EU apply to imports.

Here are just a few examples of scenarios in which the rule of origin can and cannot be applied:

How can businesses achieve reduced tariffs?

The Trade and Cooperation Agreement declares that reduced tariffs (known as preference) can be applied providing the importing business can show either a statement of origin made out by the exporter or obtain and demonstrate knowledge that the product is originating.

Claims for preference can be made upon import, but also at any time up to three years within the importation date. As such, it is essential that businesses retain accurate and comprehensive data relating to all imports.

What does the future hold?

If the rise to £4.5 billion seems steep, it could soon be eclipsed as new regulations take effect.

From 1st January 2022, the UK government implemented a new rule that businesses importing goods into the country must show a declaration relating to the origin of the goods at the point of entry.

Any company that is unable to prove the origin of their imported goods could be expected to instead pay customs duty at the standard rate as well as a fine, which many analysts expect to result in an even greater amount of customs duty being collected in 2022 and beyond.

Permalink