Every year the UK reports on its estimated lost VAT. HMRCHis Majesty's Revenue and Customs is a non-ministerial department of the UK Government responsible for the collection of taxes. has recently released their preliminary estimates of the VAT gapThe difference between the amount of VAT revenue due to a tax authority and the amount actually collected, providing insight into the difference between the VAT that should theoretically be collected and what is actually received.

HMRC publishes three estimates of the VAT gap for the latest tax year each year: the first in the autumn, the second in the spring, and the third as part of HMRC’s ‘Measuring tax gaps’ publication in the summer.

These estimates are refined over time as more economic data becomes available.

The latest update represents HMRC’s second estimate for the 2024–2025 tax year, revising the earlier preliminary figures released alongside the Autumn Budget 2025.

We expect HMRC will publish the final estimate in summer 2026, so keep an eye on this space for future updates.

What is the VAT gap?

The VAT gap is measured by comparing the net VAT total theoretical liability (VTTL) with actual receipts. This compares the amount of VAT HMRC expects to receive and the VAT HMRC actually collects.

The VTTL represents the amount of VAT that would be collected if all taxpayers complied fully with VAT legislation. By comparing this figure with actual VAT receipts, HMRC can estimate the amount of VAT lost.

To estimate the VTTL, HMRC uses a top-down methodology based on national economic data, including household consumption and spending by government, charities and other non-household sectors.

Latest estimates

For the 2024 to 2025 tax year, it is estimated the VAT gap stands at 6.5% (£11.9bn). This represents a notable increase compared to 5.0% (£8.9 billion) recorded in 2023-2024.

The estimated loss in VAT revenue has therefore grown by around £3 billion year-on-year, highlighting the ongoing challenge for tax authorities in closing the gap between expected and collected VAT.

The updated estimate is also slightly higher than the preliminary figure of 6.2% (£11.4 billion) published during the Autumn Budget 2025.

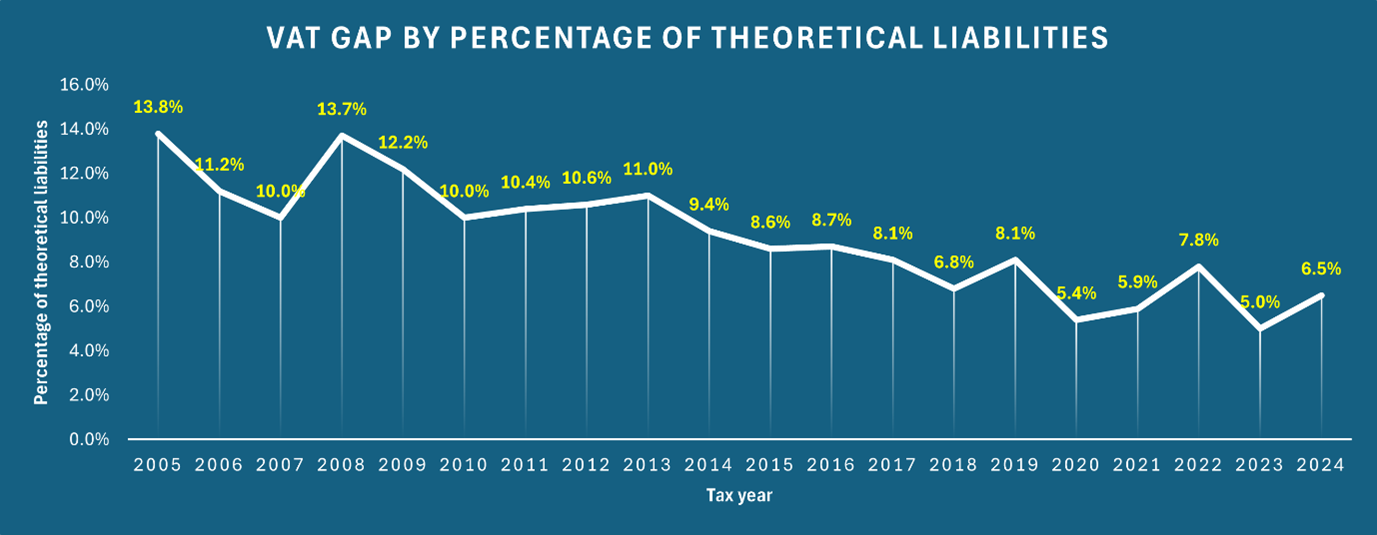

The UK VAT gap history

Despite the latest increase, the long-term trend shows a significant reduction in the VAT gap over the past two decades.

The VAT gap has fallen significantly from 13.8% theoretical VAT liability in 2005-2006 to latest estimates of 6.5%, reflecting sustained efforts by HMRC to improve compliance and modernise VAT reporting systems.

The lowest reported percentage of theoretical tax liability was in 2023 to 2024.

Recent years have seen more volatility as economic conditions and compliance challenges impact VAT collections.

How does the UK compare internationally?

The UK is not alone in facing challenges with VAT compliance. The European Commission publishes its own annual VAT gap study, ‘Mind the Gap’, which measures VAT losses across EU member states.

The most recent available figures estimate that the EU VAT gap reached €128 billion in 2023, representing a significant increase compared with the previous year.

Many European tax authorities are responding by introducing real-time digital reporting and mandatory e-invoicingElectronic invoicing - widely referred to as e-invoicing - is the exchange of a digital document between a supplier and a buyer. E-invoices are issued, transmitted and received in a structured data format that enabled automatic and electronic processing. They contain data in a machine-readable format so that an AP system can read an invoice without manual data entry, leading to faster and more efficient invoicing., which aim to improve transparency and reduce VAT leakage.

What the increase may signal

The increase in the VAT gap highlights the ongoing challenge governments face in closing the gap between expected and actual tax receipts.

Although current levels remain below the peak, the latest rise may reinforce the importance of improved compliance monitoring, digital reporting and great transparency in VAT transactions.

As tax authorities continue to digitalise tax reporting, businesses are likely to face greater scrutiny of transaction data and VAT reporting accuracy.

Actions to reduce tax gaps

One major change the UK government has announced is the introduction of mandatory B2B and B2GCommerce between business to government. e-invoicing, expected to be implemented from 2029.

E-invoicing systems allow tax authorities to receive transactional data in near real time, helping to detect discrepancies and reduce opportunities for fraud and underreporting.

The UK government believes the introduction of e-invoicing could deliver wider economic benefits, including:

- A 20% reduction in late payments

- A 3% productivity increase across financial sectors

While the mandate is still several years away, it reflects a broader global trend towards digital tax administration and continuous transaction monitoring, aimed at reducing tax gaps and improving compliance.

How we can help

With mandatory e-invoicing on the horizon, businesses should start preparing for the transition now. Our e-invoicing specialists can support you in selecting the right technology and ensuring your organisation is ready for the UK’s future e-invoicing requirements.