The countdown is on. In just a few short days both Poland and Greece launch their B2B e-invoicingElectronic invoicing - widely referred to as e-invoicing - is the exchange of a digital document between a supplier and a buyer. E-invoices are issued, transmitted and received in a structured data format that enabled automatic and electronic processing. They contain data in a machine-readable format so that an AP system can read an invoice without manual data entry, leading to faster and more efficient invoicing. mandate for large taxpayers. This comes under a wider initiative within the EU to modernise practices, curb tax evasion and streamline compliance obligations for businesses.

Greece

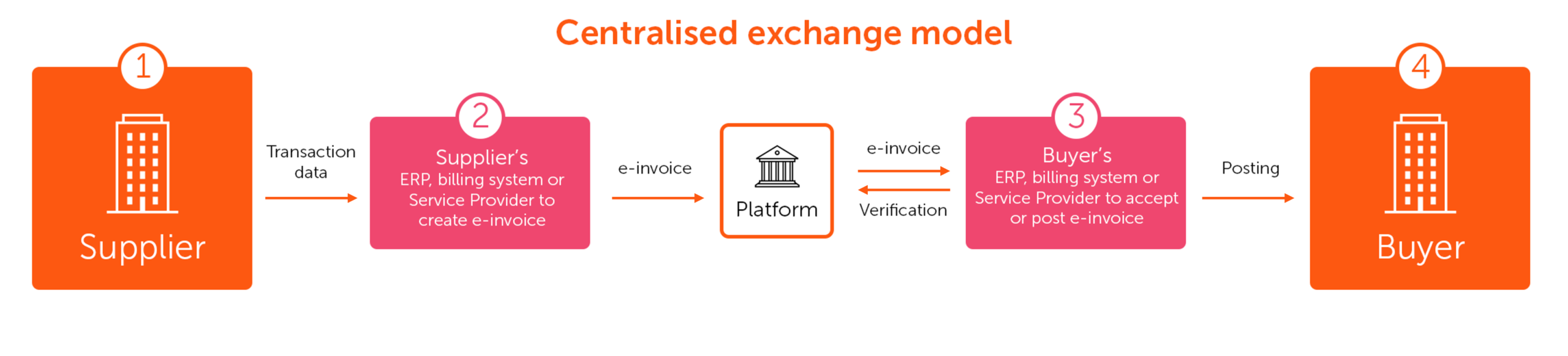

Greek taxpayers have been subject to real-time e-reporting regime since 2021, having to upload tax transactions and delivery notes to myDATA. Authorities are now launching a centralised e-invoicing model where taxpayers must use certified agents or free government applications to report. Each invoice uses a structured XMLExtensible Markup Language is a markup language and file format for storing, transmitting, and reconstructing arbitrary data. or JSON format that follows European Standard EN 16931 and is transmitted securely to AADE for verification.

AADE assigns a unique registration number (MARK) confirming the invoice’s successful reporting. This number appears on the final document shared with the buyer. All invoices are stored electronically, giving the supplier and tax authority access for monitoring and audits.

The myDATA platform or certified third-party software lets sellers generate, send, and track invoices automatically. The system removes manual paperwork, ensures data accuracy, and maintains full traceability of all transactions in Greece.

Timeline:

2nd February: Large resident companies with revenues above €1million in 2023. A gradual implementation phase will run until the end of March 2026, during which they can continue to use existing business management accounting and invoicing in parallel.

1st October: All remaining taxpayers with a transitional period lasting until year-end.

Incentives:

To encourage early adoption, companies that adopt e-invoicing two months ahead of the deadline may benefit from:

- 100% increased tax deduction for e-invoicing software and services

- Immediate depreciation of related IT equipment costs

Whilst large business can no longer benefit due to their deadline already passing, the incentives will apply to all other businesses who comply by 3rd August 2026.

Poland

Poland’s national e-invoicing system (KSeFThe National e-Invoicing System (KSeF) is for entrepreneurs in Poland to issue and receive electronic structured invoices.) transitions from concept to compulsory on 1st February. This will also operate on a centralised exchange model, requiring invoices to be issued in a structured format and transmitted through KSeF before being shared with customers.

The model introduces real-time reporting to the tax authority and increases transparency, standardisation, and control over invoicing processes. While the mandate will be phased in, businesses operating in Poland must ensure their systems, processes, and internal controls are ready to meet the new requirements.

Timeline:

1st February: Large taxpayers, over PLN 200m (2024) pa turnover.

1st April: Other taxpayers.

1st August: Bank transfer ID references must be added for KSeF.

January 2027:

- Micro businesses, invoices below PLN 450 and less than PLN 10,000 sales per month.

- Penalty regime starts for February 2026 candidates.

- Reporting of e-invoices on cash registers.

- Obligation to add KSeF numbers in transfers of invoices between businesses.

What if a company is not ready for the deadline?

Despite many companies best efforts to be prepared for the deadline,

The reasons may vary: delays on the side of IT vendors, complexity of integration with ERPEnterprise resource planning (ERP) is a type of software that organisations use to manage main business processes. systems, limited staffing resources, or unforeseen technical difficulties.

For the Polish mandate, no monetary penalties apply for breaches during 2026 under the following circumstances:

- Failure to issue a structured invoice using KSeF

- Failure to issue an invoice compliant with the invoice scheme during KSeF outage or unavailability

- Failure to submit an invoice to KSeF within the statutory deadline after the end of KSeF system outage or unavailability

However, it is important to note that the Penal Fiscal Code continues to apply in all other cases – for example, where an invoice or receipt is not issued, is issued incorrectly, or is refused to be provided.

Greece’s mandate is less clear on any financial penalty for non-compliance to the mandate, however authorities do state that you can work on existing systems in parallel with the new invoicing system until the end of March 2026. Non-compliance can result in rejected or delayed invoice processing and payment by public authorities.

How we can help

At Innovate Tax, we actively help our clients stay ahead of the evolving compliance requirements and deadlines. Our team supports businesses at every stage of the journey, from initial assessments and vendor selection to full implementations.

Whether you are preparing for your first mandatory rollout or managing multiple jurisdictions, we help reduce risk, minimise disruption, and ensure compliance from day one. Take a look at our e-invoicing services here.